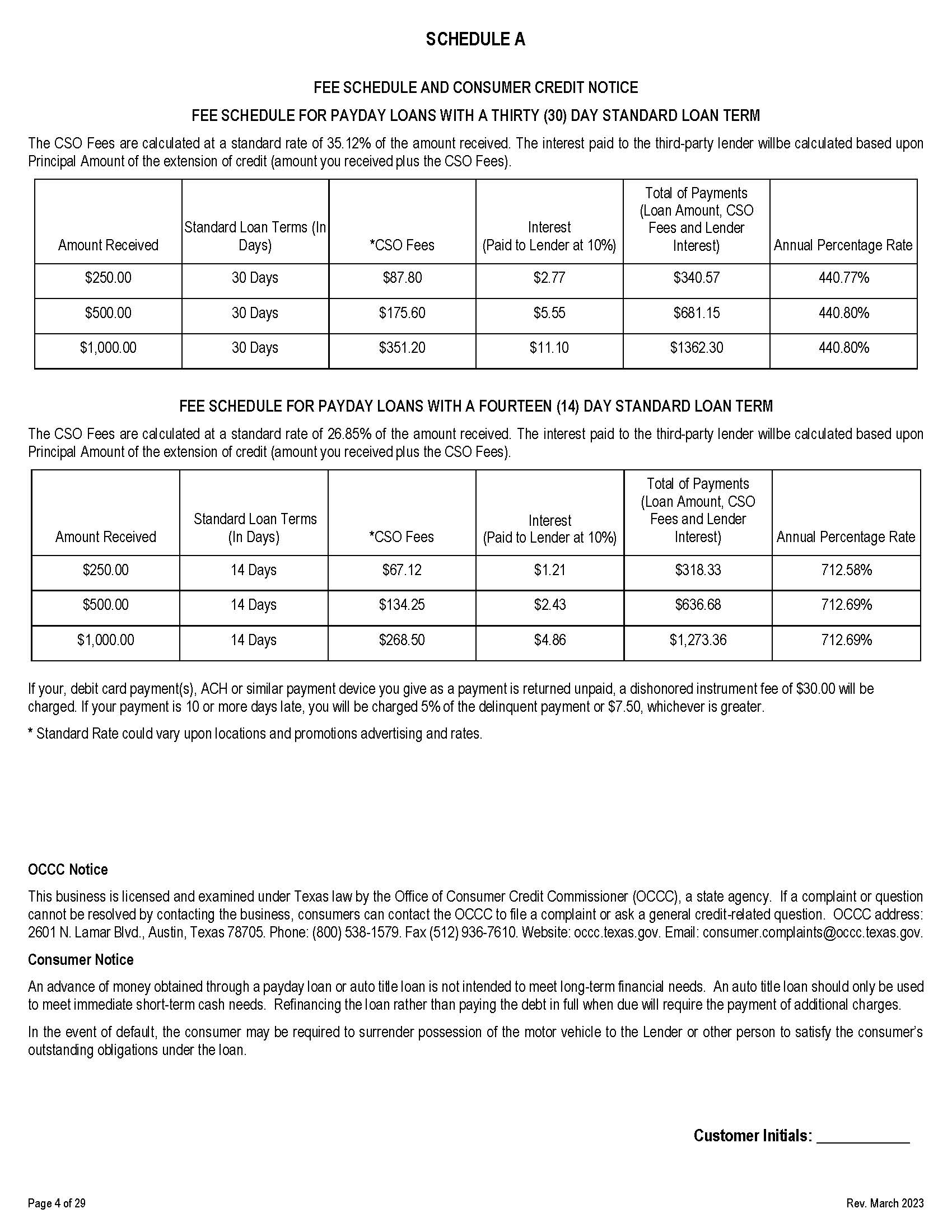

Your mastercard helps make payments seamless and you can easier, nonetheless it could also wreck your odds of bringing an aggressive mortgage if you are not careful.

While it’s true that which have a credit card can help create your credit score, it may also works up against you when it’s time for you implement to have home financing.

How does your charge card connect with your credit score?

Just as employers might use your own university GPA to evaluate their likely abilities at the office, loan providers make use of credit rating to assist determine whether you’re going to be in a position to repay a loan.

If you are searching in order to obtain, lenders tend to think about your credit score just like the indicative out-of risk – the reduced your credit rating try, the brand new riskier you look.

But it is the way you make use of mastercard that affects their overall credit score. For those who have a charge card and you will spend their bills to your go out – or, ideally, clear your debt entirely every month – it’s experienced a great indicator you’re going to be also patient in making mortgage payments.

Although not, if you don’t shell out your own expense punctually or regularly miss money, your credit score will most likely possess sustained.

Can you get home financing when you yourself have credit card loans?

Let us getting obvious, credit card debt commonly impact your residence application for the loan. But it wouldn’t fundamentally signal you from obtaining a property loan.

Some lenders are happy to provide to you personally when they can see you will be making money punctually otherwise, even better, attempting to decrease your credit card debt.

Even though some loan providers get deny your downright, anyone else might allow you pragmatic site to use from their website but within a higher rate of interest.

An experienced large financial company would be indispensable during the powering your toward lenders whose principles are a great deal more sympathetic to the individuals having borrowing card debt.

Do loan providers think about your credit limit when trying to get a house financing?

Whenever lenders determine home loan software, it test your income, expenditures, and you will existing debt agreements. Even though you don’t have tall loans on your own credit cards, they remain utilized in lenders’ data.

Centered on Put aside Financial from Australian continent investigation, Australian grownups hold typically step 1.step three playing cards, meaning many people do have more than just you to definitely. These may has actually differing constraints and you can balance however,, if these are generally put or otherwise not, of several lenders commonly check out the cumulative limit of one’s handmade cards after they assess your property application for the loan.

This may started since a shock for some as many people imagine lenders may not be also worried about cards that will be meagerly put otherwise carry little financial obligation. But that is barely the scenario.

Instead of the debt your own handmade cards carry, lenders will focus on their credit limit that they will classify given that current debt if or not you have utilized it or perhaps not. In simple terms, about attention of many loan providers, you might be ready maxing out your credit cards at any moment.

The wide variety performs

Usually of flash, a monthly bank card cost is normally regarding the dos-3% of the card’s closure harmony. Of many loan providers tend to estimate your normal mastercard payments to get 3% of your mastercard restrict.

Like, if you’ve got a credit limit away from $ten,000 round the a couple cards, lenders is also suppose the lowest payment as up to $three hundred 30 days. They’re going to incorporate this whether you’ve maxed your maximum or are obligated to pay absolutely nothing on your own mastercard levels after you fill in the application.

To grant specific tip, our credit energy calculator can also be painting an image of how their handmade cards could affect the total amount you can obtain.

Could that have several playing cards damage your residence financing odds?

Its most likely not surprising one with several playing cards normally sound security bells having loan providers, leading them to suspect you might be way of life away from function.

Due to the fact we have mentioned earlier, their bank will appear at the joint borrowing limit once you submit an application for home financing. This means that more cards you really have, the higher the brand new month-to-month credit card money their financial have a tendency to imagine you will be paying.

Whenever you are using numerous playing cards to help you organise your bank account, you could potentially consider calling the providers to reduce new limitations to the very least.

Like that, your not only set a top on the enticement to make use of the card to have some thing outside of important expenditures, but you will including set your self in the a far greater updates to acquire financing when the time comes to try to get home financing.

Must i close my handmade cards before you apply to own a home loan?

If you are looking to find a property near the top of your own credit capability, it could shell out to close your bank card profile so you can totally free upwards even more borrowing from the bank power.

Although not, if you aren’t attending get that loan to have as frequently as you’re able and you are sensibly making use of your handmade cards, it does in fact work facing one to personal the credit card membership, due to the fact we’re going to explore lower than.

However, when you’re having your money in order to sign up for an effective home loan, you need to obvious as often personal credit card debt since you fairly is also minimizing new limitations on each credit.

Overusing handmade cards plunges your credit rating

It has to forgo saying that when you find yourself with your borrowing from the bank cards willy-nilly and you can destroyed repayments, otherwise you’re regularly exceeding the cards constraints, your credit score will be using struck. Obviously, this may enchantment troubles after you submit an application for home financing.

Normally your own bank card use enhance your likelihood of getting approved for a mortgage?

With your mastercard can actually alter your credit history, but only if you are doing it with alerting. Spending money on requests together with your cards and you can repaying the balance on the go out shows a confident cost development so you can possible loan providers.

When you have established credit card debt, attempt to shell out over minimal monthly premiums every day. It may also be really worth inquiring your own mastercard provider so you can reduce your restriction into low part you to definitely however matches you means.

It-all comes down to showing that you’re in charge. Loan providers want to see as you are able to deal with debt and you will would your bank account well, thus consider one to before you use your charge card.

If you are concerned their charge card use you can expect to impede their dreams of shopping for property, you could potentially seek out a large financial company to own personalised recommendations so you can assist in their borrowing stamina. They might and additionally support you in finding loan providers who’re more stimulating on the credit card explore.

Mastercard or otherwise not, all the homebuyers was aiming to hold the lowest financial notice speed offered to them. If you are trying to find a home loan, below are a few of the greatest offers around at this time: